copy of income tax tribunal order

posted by mody at 1:37 PM

![]()

![]()

SYNOPSIS 1.Has raised tax demand on assumption basis from family members. 2. Senior tax officials has not furnished all necessary documentary evidences as well as written statement of auditors,Jalundhwala ,etc. (3)Has used means of harassment and coercion to collect taxes from my wife and my children. (4)Need to get back refund back. (5) Need to obtain all documentary evidence.

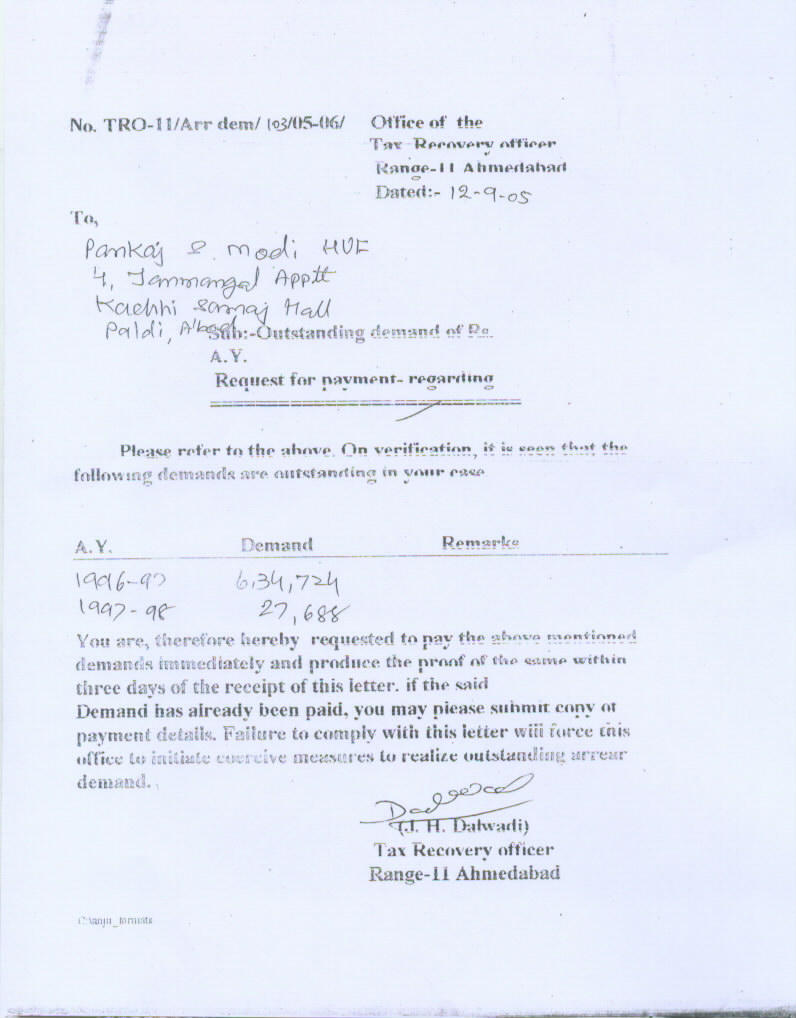

Letter from Tax Recovery Officer , Range 11 dated 12-9-2005 received on 30-9-2005.

posted by mody at 4:36 PM

![]()

![]()

From:

Pankaj S Mody

C/o Shri Suresh S Modi

Janmangal Apt ,

2nd floor

Paldi ,

Ahmedabad 380 006

DATED 12-9-2005

The Assessing Officer , Ward 11 (2)

Narayan Chambers ,

Ashram Road

Sir,

This is in reference to your communication dated 1-9-2005. At the outset let me make it clear that I do not have any taxable income and nor am I in position to engage services of a tax consultant.

I humbly request you to provide detailed findings as well as action taken report in light of my various letters addressed to the predecessor assessing officers as well as to Tax Recovery Officers and others especially when he matter is pending since long. Amongst various issues , I have referred to the statement made by assessing officer for assessment order passed in March 2002 and the same is referred as under:- - “Details were calledfrom Dhanyushya as all the details are in its possession in respect of transfer ofshares. Details have not been received from DFPL and hence it is not possibleto give finding in respect of exact date of transfer of shares along withcompleted share transfer deed.” Primarily it is duty of the assessing officer to collect such information from the other parties with a view to provide natural justice to me. Till date , the office of Assessing Officer has not done this for obvious reasons of extending favour to Dhanysuhsya and connected associated persons. It is also apparent from the audited balance sheet of Dhanyushya for the period ending March 31-3-97 that , they do not own any of my shares of Rupmanglam and Flovin as the same is not reflected in their balance sheet.

You would appreciate that I have my natural as well as fundamental right to Information and as long as you do not provide detailed findings , it is not proper on your part to call for any information from me. Besides there is on going inquiry by Police Authorities of Gujarat in light of my complaint and hence you cannot demand cooperation from me till you furnish detailed findings and permit me to cross examine Dhanysuhaya.

Amongst various letters addressed to Assessing Officer as well as to the tax recovery officer from time to time , kindly refer my letter dated 17th Oct 2003 addressed to the Assessing Officer. Till date , I have not received any reply from your end in this regard. This is not fair and besides your indifference shows that the assessing officer lacks sensitivity for the common citizens.

When the information has not been received , with a view to provide natural justice , it becomes your responsibility to collect the details from Dhanyushya as assessing officer and if you fail to do so then it is either deficiency in services and/or that you are extending undue favour to protect Dhanyushaya , their directors , chartered accountants as well as tax advocates This would naturally attract provisions of Corruption Act against all the concerned officials of the Income tax department .

I have been advised by letter dated 26-12-2000 ( HQ.III/101-M-26/Form.No.34A.AR.8/2000-2001 from the Commissioner of Income Tax –III (P C Verma) , Ahmedabad that the assessing officers have been given appropriate instructions. Please let me know the circumstances under which the income tax clearance certificate was given in a hot hurry and the steps taken by you to attach the bunglow for approving sale consideration which is lower than purchase price and when there 37 I permission has not been obtained.

I am marking a copy of present letter to concerned authorities as to why action should not be initiated against you for extending favour to Dhanyushaya and its directors, chartered accountants, tax consultants and escrows by furnishing their reply to me , in case you do not furnish satisfactory detailed findings and action taken report against this group. You must be aware that the action has been initiated against the management of Core Health care and others by Anti Corruption Bureau in light of directions given by the Sessions Court.

It is in your interest to rectify the situation by taking suitable action and reporting findings and avoid having herd mentality. In interest of natural justice , it is necessary that you furnish the detailed findings to me at my email address. I reserve my right to raise other issues at a later stage as and when necessary.

Kindly furnish detailed findings and action taken report to the undersigned at my email address modyps@gmail.com and to the Home Department pshome@gujarat.gov.in forthwith so that various provisions of extending favour to Dhanyushaya are not attracted against you. In case,you fail to furnish such information to me and the Home department forthwith , then various provisions of extending favours to Dhansyuhsya , their auditors and tax consultants and directors,etc would be applicable to you, which please note. I do hope that you would not like to be placed in such an embarrassing situation for deficiency in services on your part. A copy of present letter is being sent to them for their knowledge and action in case you fail to furnish such details to them.

Thanking you.

Yours sincerely,

Pankaj S Mody

Enclosure:-

1. Copy of audited b/s of Dhanyushya for period ending March 1997.

2. Sandesh article dated 25-8-2005 on Core Health care management .

3. Income tax clearance certificate issued in year 2000 by the then assessing officer.

4. Copy of letter dated 17-10-2003 addressed to Assessing Officer.

posted by mody at 4:43 PM

![]()

![]()

posted by mody at 4:45 AM

![]()

![]()

posted by mody at 6:07 PM

![]()

![]()

NOTICE OF DEMAND TO THE DEFAULTER

NO TRO-11//180/II /2004-05 OFFICE OF THE TAX RECOVERY OFFICER

RANGE –11 , ROOM NO –111

1ST FLOOR ,NARAYAN CHAMBERS

NEHRU BRIDGE

ASHRAM ROAD, AHMEDABAD

DATED 06-01-2005

To,

Shri Pankaj S Modi Huf

4 Janmangal Apt

kachi Samaj Hall

Nr. Sharda Mandir Crossing

Paldi < Ahmedabad

This is to inform you that a sum of Rs 06,37,724 dues from you for A.Y. 96-97

Rs 12,95,268 dues from you for A.Y. 97-98

Rs 8,480 dues from you for Ay 98-99

Rs 5,640 dues from you for AY 99-00

2. In this connection, you are requested to pay up the arrear demand immediately failing which the recovery proceedings will be started in accordance with the provisions of section 222 to section 232 of the income tax act , 1961 and the seconds schedule to the said act and the rules made thereunder. If you have anything to be clarified in thematter, you are requested to personally attend my office ( if necessary alongwith your authorized representative ) at the above4 mentioned address on 27-01-2005 at 11:30 AM for a personal hearing.

3. In addition to the sum aforesaid, you will be also liable for:-

(a) such interest as is payable in accordance with sub-section (2) of section 220 of the said Act for the period commencing immediately after the issue of this notice.

(b) All costs charges and expenses incurred in respect of the service of this notice and of warrants and other processes all other proceedings taken for realizing the arrears.

S/D

J H DALWADI

TAX RECOVERY OFFICER

RANGE-11, AHMEDABAD

posted by mody at 7:35 PM

![]()

![]()

Pankaj S. Mody

c/o Shri S.S. Modi

40 BMM Society

Paldi

Ahmedabad 380 006

EMAIL:- psmody@yahoo.com

02-12-2004

The Commissioner of Income-Tax-Appeals (XVII)

Nature View Building

Near H K House

Ashram Road

Ahmdebad

Respected Sir,

SUB: THE APPEALS PENDING BEFORE YOU AS REGARDS TO PERSONAL AS WELL as HUF for the assessment year 96-97 and 97-98 for hearing on26-10-2004

REFERENCE :- MY EARLIER CORRESPONDENCE LETTERS 25-10-2004, 18-08-2004 AND 24-02-2004

I am in receipt of the notice of hearing in my case for assessment years 96-97 and assessment years 97-98 fixed for hearing on 6-12-2004.

In this connection, I the undersigned humbly make to invite your Honor’s kind attention to my request letter/petition dated 24-2-2004,18-08-2004, 25-10-2004 addressed to your Honour. I hereby state that I have not received any reply in this matter. Consequently , Kindly note that it is not possible for me to appear before your good self because I have raised several critical and

relevant issues in my above referred petition letters addressed to your Honour and unless I am equipped with the clarification and reply , it will not be possible for me to defend my case and consequently, such action on your part will have the effect of violating the principals of natural justice ,which , I am sure will not like you to be instrumental to the injustice which is likely to be caused to me if the appeal is decided in my absence. Besides, the issue of GTB as well as conduct of great robber Mr. Sushil Handa is involved. Under no circumstances, you can turn a blind eye to the events.

In view of the above mentioned facts and the circumstances of the case, I request your good self to give a long adjournment in this case and favour me with the reply to my impugned petition letters dated. 24-2-2004 , 18-08-2004 and 25-10-2004.

An early reply will meet with the ends of justice.

Thanking you.

Yours most obediently,

Pankaj S Mody

Enclosure: Copy of email on 26-10-2004 to The President of India

“ ALL THAT IS NECESSARY FOR THE TRIUMPH OF EVIL IS THAT GOOD MEN DO NOTHING- EDMUND BURK

“ The evil of the world is made possible by nothing but the sanction you give it - Ayan Rand

posted by mody at 5:45 PM

![]()

![]()

By Speed Post

PANKAJ S MODY

C/O SHRI S S MODI

40 BMM SOCIETY

PALDI ,

AHMEDABAD 380 006

Email id : psmody@yahoo.com

October 25, 2004

The Commissioner of Income Tax-Appeals (XVII)

Nature View Building

Near H K House

Ashram Road

Ahmedabad

Respected Sir,

Sub: the appeals pending before you as regards to personal as well as HUF for the assessment year 96-97 and 97-98 fixed for hearing on 26-10-2 004

Reference :- my earlier correspondence letters dated 18-08-2004 and 24-02-2004 .

1. This is in reference to above the hearing fixed on 26-10-2004.

2. I am unable to take out some of the relevant files as the residence of my my parents is closed as my mother is being operated . Hence, kindly grant a fresh date after two weeks as till then I would not be able to appear before you.

3. In light of my above letter dated 18-08-2004 , I once again humbly request you to arrange for appellate orders passed in case of my wife Mrs S. P. Mody and my children as the facts and circumstances of the case are identical and my family members are not extending cooperation as informed to the department as well as to you during the discussions.

4. I fail to understand as to how the appellate orders have been passed without collecting necessary facts by collecting necessary documentary evidence and recording statement of Dhanyushya Financial , Jatin Jalundhwala, Mr. Saurabh Soparkar, Mr. Hemant Kashiparekh and M/s Shah and Shah Associates especially when my family members had specifically requested the –then assessing officer. It is absolutely clear that some one from the department is protecting these persons even if it results in loss of revenue from these persons/companies/tax advocates/chartered accountants.

5. You would appreciate that , the department needs to extend full cooperation as I am the one who is the informant-cum- whistleblower of tax evasion and it is necessary that all the facts and documentary evidence are furnished to me in view of natural justice, equity and good conscience.

6. Human consideration and approach need to be followed by the income tax department as under no circumstances the right to information can be denied to me in a democratic country as it unnecessarily involves cost of litigation, hardship to the assessee and this is nothing but barbaric methods being employed in a civilized society to use methods of coercion to extract taxes by hook and crook from the citizens of the country.

7. In case you are facing some hurdles , it would be better that you write top Prime Minister of India and make representation to him that the circumstances require to have transparent approach even if it may involve exposing the misconduct of the officials involved in the assessment as well that of Investigation department. It is natural to expect such respect and conduct from the top officials of the Income tax department.

8. As the assessing officer and his peers as well as his superiors has used means of coercion to extort taxes from my family members on my complaint against some of the senior officers of the department to the Central Vigilance Commission , I do not have any option but to mark a copy of my present letter to the President of India presidentofindia@rb.nic.in as well as to the well known columnist of Indian Express Tavleen Singh at tavleensingh@expressindia.com

9. In the wider and broader interest of revenue , it is necessary that you call for complete documentary evidence from Mr. Jatin Jalundhwala , Mr. Hemant kahiparekh , Mr. Saurabh Soparkar and M/s Shah and Shah Associates without any further delay.

10. You may have a look at some of the correspondence with the income tax department by visiting site http://www.intad.blogspot.com and excerpt of book published by media which deals with the state of affairs in the income tax department as referred in the link http://www.redtrapism.blogspot.com

11. I look forward to your whole hearted support and cooperation and I would prefer reply to my email address as I do not have any correspondence address for about a fortnight as my parents would not be available at the above residence so that they can inform me.

YOURS sincerely,

Pankaj S Mody

posted by mody at 11:10 AM

![]()

![]()

Pankaj S Mody

C/o Shri S S Modi

40 BMM society

Paldi ,

Ahmedabad 6

Email id: psmody@yahoo.com

October 11,2004

To

posted by mody at 3:20 PM

![]()

![]()

posted by mody at 2:08 PM

![]()

![]()

posted by mody at 8:22 PM

![]()

![]()

I humbly request you to call for detailed action taken report and detailed findings pursuant to my letters addressed to the officials of the income tax department by fax

so that you can personally verify indifference, sloth, inefficiencies prevailing in the department and the tricks employed by the officials to harass parties.

REPLIES , ACTION TAKEN REPORT AND DETAILED FINDINGS PENDING BY THE UNDERMENTIONED SENIOR OFFICERSWHILE CAUSING GREAT HARASSMENT TO THE COMPLAINANT .

SRNO DESIGNATION NAME REPLY PENDING REFERENCE ACTION REQUIRED

1 DIRECTOR GENERAL OF INCOME TAX-INVESTIATION, AHMEDABAD FAX 079-27545776, phone 079-27546645 UDAY PRATAP SINGH:- APPLICANT’ LETTER 3-3-03 AND TELEGRAM DATED 10-3-03 .HAS NOT TAKEN DETAILED ACTION PURSUANT TO THEIR REF FILE DG/AHD/INV/29/99-2000 DATED 19-9-2000 TO CALL FOR ACTION TAKEN REPORT AND DETAILEDFINDINGS TO ALL THE LETTERS

2 DIRECTOR OF INVESTIGATION,AHMEDABAD Fax: 079-27546192, office: 079-2754603 APPLICANT LETTER DATED 4-7-2001 ENCLOSING LETTER 2-7-2001 TO CALL FOR DETAILED FINDINGS

3 ADDITIONAL DIRECTOR OF INCOME TAX,AHMEDABAD Fax: 079-27646559,office-079-27546645HE IS IN CHARGE OF WING UNIT 1(3) AND UNIT 1(4)

4 CHIEF COMMISSIONER OF INCOME TAX-III , AHMEDABAD Fax: 079-27544287,office 079-27546244-7101 R. B. SHUKLA APPLICANT LETTERS DATED 3-3-03 WHICH HAS BEEN JOINTLY ADDRESSED TO PREDCESSOR CCIT AND CURRENT LETTER DATED 3-9-03 TO CALL FOR DETAILED FINDINGS

5 COMMISSIONER OF INCOME TAX-V AHMEDABAD Fax: 079-27546253, office: 079-26576382M C KATHERIYA NOT CONDUCTED INQUIRY TO APPLICANT LETTER TO CONTENTS OF LETTER DATED 16-12-2002, 3-6-2003, 4-6-2003 TO CALL FOR DETAILED INQUIRY REPORT

6 ADDITIONAL COMMISSIONER OF INCOME TAX-RANGE 11 , AHMEDABAD

Fax: 079-26741686, office 26584535 M H PANDAV HAS NOT FURNISHED DETAILED REPLY TO LETTER 17-10-2002 TO CALL FOR RESULTS DETAILED FINDINGS

7 ASSESSING OFFICER –11(2) R.N.RAWAL NOT REPLIED TO LETTER DATED 12-2-03 TO HIS PREDECESSOR ASSESSING OFFICER TO CALL FOR DETAILED INQUIRY REPORT

8 CURRENT ADDITIONAL CIT.,AHMEDABAD FAX 079-27546253, PHONE: 079-27546253 RAJEEV NABAR HAS NOT REPLIED LETTER 24-1-02 AS JCIT RANGE 1 TO CALL FOR DETAILEDFINDINGS

posted by mody at 8:37 PM

![]()

![]()

ANNEXURE I: LIST OF SOME CORRESPONDENCE LETTERS WITH INCOME TAX DEPARTMENT,IN AHMEDABAD

SR NO DATE OF

CORRESPOND ADDRESSED TO WHOM STATUS

1 18-6-1999 TO CCIT AND DGIT-INVEST

2 REMINDER OF ABOVE LETTER

3 REMINDER OF 18-6-1999 LETTER

4 29-3-2000 TO DDIT UNIT 1(4) R.DIWEDI

5 11-5-2000 TO DDIT UNIT 1(4) R. DIWEDI

6 24-7-2000 TO DGIT

7 15-9-2000 TELEGERAM TO DGIT

8 19-9-2000 LETTER TO MODY BY DGIT ON 19-9-2000

CONFIRMING MY ALLEGATIONS AS REFERRED

IN LETTER DATED 18-6-99

9 3-10-2000 LETTER TO DGIT NO REPLY

10 23-10 –2000 LETTER TO DGIT NO REPLY

11 30-10-2000 LETTER TO DGIT NO REPLY

12 27-11-2000 LETTER TO DGIT NO REPLY

13 14-12-2000 TELEGRAM TO DGIT NO REPLY

14 4-1-2001 TELEGRAM TO DGIT NO REPLY

15 20-1-2001 TELEGRAM TO CCIT NO REPLY

16 15-3-2001 TELEGRAM TO DGIT NO REPLY

17 4-6-2001 LETTER TO DGIT NO REPLY

18 2-7-2001 LETTER TO DDIT UNIT 1(4) NO REPLY

19 4-7-2001 COPY OF ABOVE LETTER MARKED TO DIT NO REPLY

20 29-10-2001 LETTER TO JCIT –RANGE 1 NO REPLY

21 23-01-2002 LETTER TO DGIT NO REPLY

22 24-1-2002 LETTER TO JCIT RANGE 1 NO REPLY

23 10-6-2002 LETTER TO CENTRAL VIGILANCE COMMISSION

dated 3-6-2002 endorsing COPY TO DGIT on

10-6-2002 AND CBDT NO REPLY

24 25-6-2002 LETTER TO DGIT NO REPLY

25 17-10-2002 LETTER TO ADCIT –RANGE 11, MR. PANDAV

REJECTED REQUEST FOR STAY OF DEMAND

without GIVING ANY REASONING

26 18-10-2002 LETTER FROM DIRECTOR OF INCOME TAX

(VIGILANCE)

F.NO. DIT(V) (W) /CON-166/U-II/2002-03

finding to my letter dated 31-10-2002

and fax dated 14-11-2002 HAS NOT BEEN

FURNISHED

27 16-12-2002 LETTER TO CIT-V No reply

28 30-12-2002 LETTER TO DDIT UNIT1(3) GAVE REPLY

ON 29-1-2002 REPLIED THAT

ASSESSING OFFICER

WOULD GIVE REPLY

29 10-1-2003 LETTER TO RANGE 8 NO REPLY

posted by mody at 7:25 PM

![]()

![]()

posted by mody at 4:31 PM

![]()

![]()

posted by mody at 3:57 PM

![]()

![]()